KSE Institute’s Russia Chartbook – The Russian Economy At The Start Of 2025: Underlying Vulnerabilities, Depleted Macro Buffers, But No Signs Of An Immediate Crisis

28 January 2025

KSE Institute has released its new January Russia Chartbook “The Russian Economy At The Start Of 2025: Underlying Vulnerabilities, Depleted Macro Buffers, But No Signs Of An Immediate Crisis.” Ukraine’s allies must maintain a coordinated and consistent approach to uncover Russia’s economic vulnerabilities, further complicating its economic management.

Russia’s external environment remained supportive in 2024, with a current account surplus of $53.9 billion, slightly exceeding $50.1 billion in 2023. However, the surplus weakened significantly in the second half of the year, falling to $12.6 billion from $41.3 billion in the first half. Goods imports rose by $19 billion in the second half, while service and income transfer deficits increased by $5 billion each. Oil and gas exports grew by 2%, adding $6 billion due to higher prices, but exports of other goods declined by 7%, resulting in a $13 billion loss.

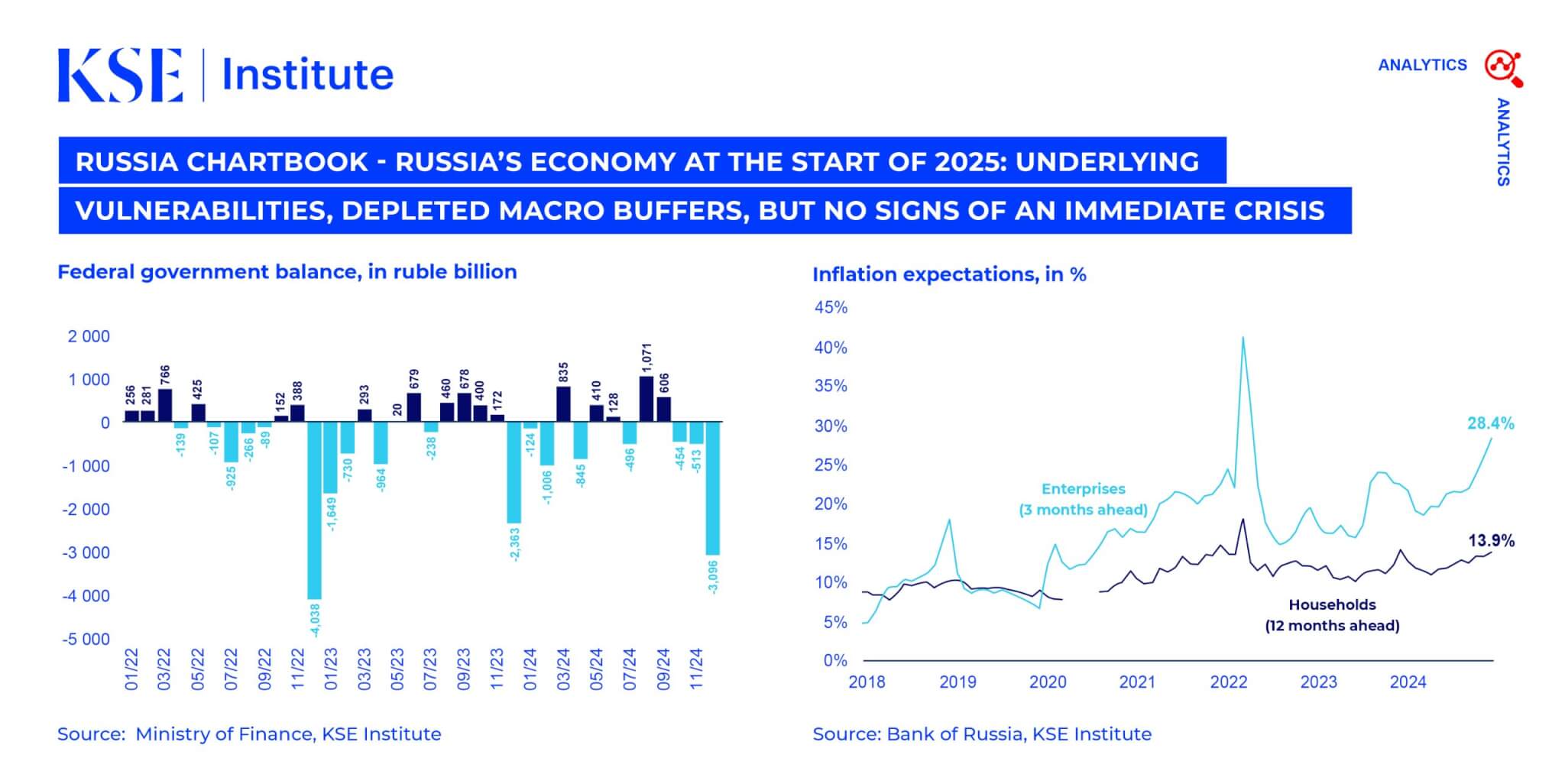

The federal budget deficit in 2024 reached 3.5 trillion rubles, equivalent to 1.7% of GDP or about $39 billion. This aligns with the deficits of the previous two years in ruble terms. Revenues from oil, gas, and non-oil sectors increased by 26% compared to 2023, helping to offset a 24% rise in spending. Despite this, the full-year deficit significantly exceeded the planned 1.6 trillion rubles. In December, the 3.1 trillion ruble deficit was financed through a 1.3 trillion ruble transfer from the National Welfare Fund and 2 trillion rubles in domestic debt issuance, supported by a Central Bank repo operation.

Russia’s macroeconomic buffers remain under pressure. The liquid assets of the National Welfare Fund have declined to 3.8 trillion rubles, a 60% drop since February 2022. With hard currency reserves depleted by the end of 2023, Russia sold yuan-denominated assets and gold in December to cover the budget deficit. At current prices and exchange rates, the fund’s liquid assets amount to $37.5 billion, which are close to depletion for budgetary needs. Meanwhile, an estimated $340 billion of Central Bank reserves remain frozen due to sanctions, limiting monetary policy options, with the location of approximately 85% of these assets identified.

While the Russian economy faces serious vulnerabilities, there is no immediate crisis. GDP growth in 2024 is estimated at around 3.5%, similar to 2023. This growth was supported by increased government spending on the war, a surge in private sector bank loans, and a tight labor market. However, these factors, along with ongoing ruble depreciation, pushed inflation to 9.5% year-over-year in December. Despite the Central Bank’s significant interest rate hikes of 1,350 basis points since mid-2023, inflation remains high due to compromised monetary policy transmission.